Why we need Decred: A sound money with voice

What is sound money, and how is it related to Bitcoin? Why do our currencies lose value over time? Can we automate politics out of monetary policy making, but retain a structure for coordination and governance?

Abstract: This research paper outlines how Bitcoin is a rethinking of traditional currencies. Readers will learn how currencies are a form of monetary sovereignty, and how different schools of economics and governance shape the world’s leading reserve currencies. By studying the Euro, the US Dollar, and the IMF’s Special Drawing Rights, this paper articulates a framework to understand how Decred is a unique cryptocurrency which builds on the economic properties of Bitcoin with additional means of cooperation and conflict resolution. As a key takeaway, readers will learn how Bitcoin is more than a digital cash, and Decred is more than Bitcoin.

Table of Contents

- Currencies are a form of sovereignty

- A quest for Sound Money: Keynesian Economics vs Austrian Economics

- Currency Governance: Examining the decision making processes in the Euro, the US Dollar, and the IMF Special Drawing Rights

- Bitcoin is a transformative innovation over traditional currencies, but it lacks clear governance

- Decred builds on Bitcoin’s design with a more inclusive approach to sound money

- Decred is still nascent — Weaknesses, misconceptions and opportunities for the future

Currencies are a form of sovereignty

What is money, anyways? Our older ancestors used precious stones and metals as money, and until a few decades ago, our government money had to be backed by gold. Since the 1970s, the world has used a system of fiat currencies which are backed by government promises, rather than an intrinsically valuable commodity.

Today, the United Nations recognizes 180 different currencies in 195 nations around the world. Most countries issue their own currencies, even though economists acknowledge that currency exchange fees create transaction costs. This is because having your own national currency provides us a form of monetary sovereignty, rather than having to depend on a currency issued by a different country. As an example, 90 percent of Canada’s population lives within 100 miles of the US border, but Canada issues its own currency, the Canadian Dollar.

While most countries issue their own currencies, the Euro and the US Dollar have been adopted by multiple countries as official legal tender. As of 2020, the Euro is the official currency of 19 European nations, and the US Dollar is the official currency of 7 countries. The wide adoption of these two currencies also makes them ideal candidates to be held in the reserves of other central banks. The majority of countries around the world have also agreed to constrain their monetary sovereignty by agreeing to abide by Articles of Agreement of the International Monetary Fund. In essence, they have traded off monetary sovereignty in exchange for “international cooperation and for the common good of all”.

When countries in the Eurozone ceded their monetary sovereignty to the European Central Bank, they did so after establishing a governance framework where they could retain a voice at the ECB. Similar means of governance also exist at the International Monetary Fund, which will be unpacked later in this paper.

With the advent of cryptocurrencies, we now have digitally native currencies which are no longer bound by our offline borders. Software is eating the world, and cryptocurrencies allow us to program monetary policies into money as a software. This opportunity also comes with questions about the ideal characteristics of money as a product, along with differing approaches to monetary economics.

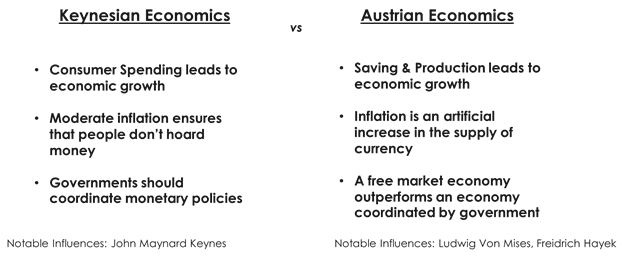

Keynesian Economics vs Austrian Economics — in search of sound money

Is it better to save, or to spend? Depends on who you ask. Some economists believe in consumption, while others believe in savings and production. These competing theories of money prioritize different features in their ideal design of money.

Keynesian economists believe that consumer spending, guided by government coordination and light inflation is the key to economic progress. A key premise in Keynesian school of thought is that if people know their currency will be worth less in the future, they will be more incentivized to spend money today, which will lead to greater money circulation. This school of thought dominates global economics today, and even our economic measures like GDP use spending as a proxy for national prosperity.

If Keynesians are spenders, Austrian economists are savers. Austrians believe that money should retain its value over time, and political interventions in monetary policy leads to short term bubbles and longer term losses.

Nobel laureate Freidrich Hayek compared government monetary creation to the pouring of honey in a cup. The honey tends to clump in the center, and unevenly trickle out to the outer ridges.

When central banks are able to increase the money supply at will, the value of the currency inherently loses purchasing power. We don’t realize this right away, but over time, this leads to price inflation in everything we buy. Rising asset prices benefit the people who hold capital investments, but life becomes more more expensive for those who live on cash savings.

Inflation distorts our ability to measure prices over time, and disproportionately harms the poor. But our currencies don’t always have to lose value over time. Advocates of sound money believe that a stable currency would lead to societal prosperity, as our savings would be protected from debasement. Over time, a change in prices would come not from currency supply increases, but from productivity gains realized by technology.

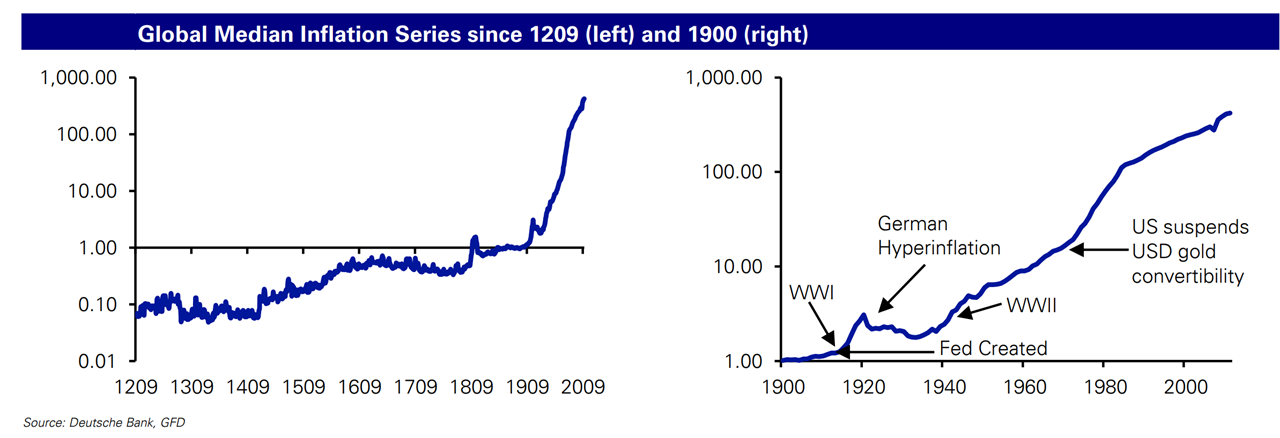

The concept of sound money may be new to many people, because we’ve lived our entire lives under a system of fiat currency with central banking oversight. But life wasn’t always like this. Seen under a historical economic lens, central bank oversight with fiat currencies is a relatively recent phenomena, which has also coincided with history’s largest bouts of hyperinflation:

Over the last century, even the US Dollar (the world’s strongest national currency) has lost more than 95 percent of its value due to inflation. Because our money loses value, we are incentivized to move our net worth out of cash. This has given rise to a culture of consumption, as well as complex financial providers who extract fees in exchange for protecting against inflation.

Sound money is a money which is not subject to inflation and supply fluctuations. To most 19th century writers, sound money is synonymous with gold, because of its well known scarcity and durability. At any given time, there is only a finite amount of gold that ever exists on earth, and most of the gold mined in history still exists today.

Where sound money optimizes for value and price stability, fiat money enables greater national economic coordination. By retaining a voice over their monetary policy, nations are able to fund social programs, which can especially helpful during economic downturns.

Understanding the coordination frameworks for the world’s leading currencies can offer us valuable insights about the role of governance in our economic institutions.

Comparing the role of governance in the Euro, the US Dollar, and the IMF Special Drawing Rights

The Euro:

The Euro is the best known modern supranational currency, where a single unit of account is the legal tender for multiple nations.

The concept of a monetary union among European countries has been explored since the 1960s. In the early 1990s, an alliance of European countries formally proposed action to adopt a common currency, recognizing that this would remove exchange rate barriers and enable more free flowing trade. The European Central Bank was created in 1999, which formalized the creation of the Euro as a single currency which is now the legal tender for 19 countries.

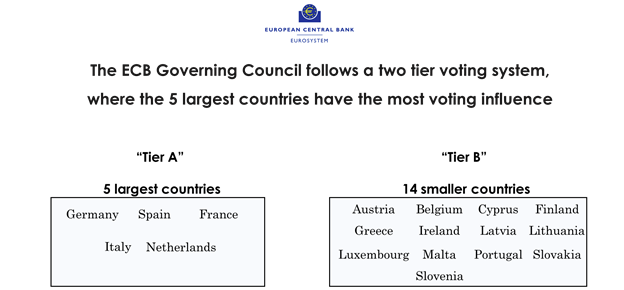

When Eurozone countries ceded Monetary policy to the ECB, they did so with the implementation of a means of governance. The ECB Governing Council is the main decision-making body of the Euro. It consists of

- 6 members of the ECB Executive Board, plus

- 19 national central bank governors

Voting power in the European Central Bank reflects those with the most skin in the game:

While the Euro is the adopted currency of 19 countries, the voting power of the ECB does not follow a ‘one person one vote’ framework. The governing powers of ECB countries are divided into groups according to the size of their economies and their financial sectors.

Voting power in the ECB Governing Council reflects the national economies with the most skin in the game.

For decision making in the ECB Governance Council, the Governors from the 5 largest economies — currently, Germany, France, Italy, Spain and the Netherlands — share four voting rights. The 14 other countries share 11 votes, where their governors rotate turns on a monthly rotation. On a monthly basis, consensus is reached after voting as follows:

· The 6 members of the ECB Executive board each casts 1 vote

· The 5 biggest countries take turns sharing 4 votes

· The 14 smaller countries take turns sharing 11 votes

How voting rights rotate on the ECB Governing Council

The accession of Lithuania as the euro area's 19th member state as from the beginning of 2015 will trigger a new voting…

www.bundesbank.de

The Governors of the ECB meet to set interest rates, monitor the money supply, and assess how participating populations can enhance their economic coordination. A similar framework also exists in the United States.

The US Dollar and the Federal Reserve:

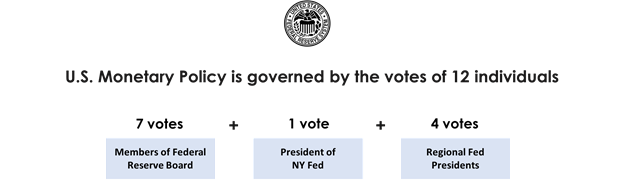

While the Euro is governed by the ECB, the US Dollar is governed by the US Federal Reserve. Much like the ECB has a governing council, the Fed’s monetary policy is governed by the Federal Open Market Committee (FOMC). The FOMC has 12 voting representatives:

- 7 board members of the Federal Reserve System (appointed by the US President with the approval of the Senate).

- 5 members are presidents of the twelve regional reserve Banks.

Much like the five largest countries enjoy preferential voting treatment in the European Central Bank, the New York Fed also enjoys a preferential treatment in the form of a permanent voting status, owing to New York’s central position in American finance. The presidents of the remaining 11 regional federal reserve banks share 4 votes on a rotating basis.

The US Dollar is the current reserve currency of the world, and most trade is conducted in dollars. When the 12 members of the FOMC make monetary policy decisions, they also inherently have governance rights over the foreign exchange reserves for every other country holding the US Dollar. To address this inherent conflict of interest, and to supplement the global supply of dollars, in the 1960s the IMF created the Special Drawing Rights.

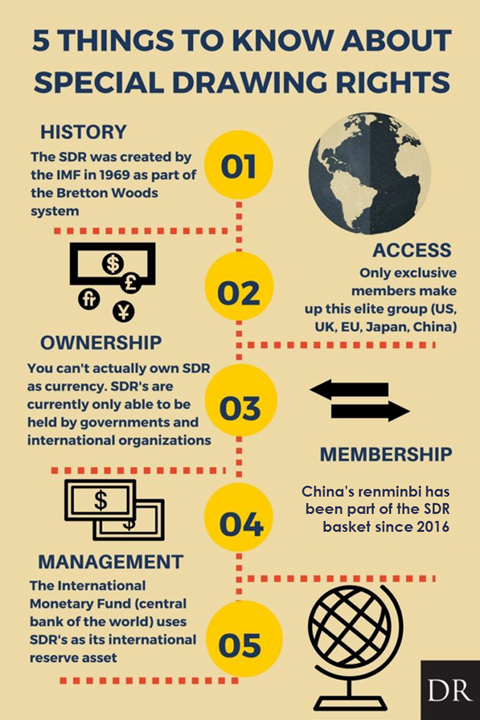

The Special Drawing Rights — an international reserve asset

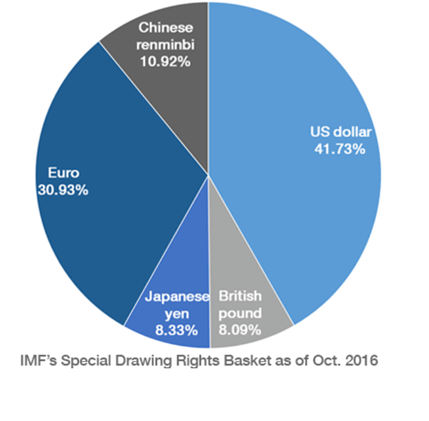

The currencies which makeup the SDR are a proxy for the influence of the largest economic influences in the world. The basket is reviewed every five years to ensure that it reflects the relative importance of global currencies and financial systems. Deriving the SDR value from a basket model helps manage against exchange volatility in any single currency.

SDRs were introduced in the late 1960s as a common global reserve asset, with their value being pegged to gold via the US dollar under the Bretton Woods system. The US ending its dollar convertibility into gold lessened the importance of the SDRs in global economics.

Today one of the main functions of the SDR is to serve as a unit of account for the International Monetary Fund (IMF), the Bank for International Settlements (BIS), Arab Monetary Fund, African Development Bank, and the Islamic Development Bank. A few countries also peg their currency to the SDR.

Special Drawing Rights Governance — Voting power with skin in the game

“Unlike the General Assembly of the United Nations, where each country has one vote, decision making at the IMF was designed to reflect the relative positions of its member countries in the global economy. Each IMF member country is assigned a quota that determines its financial commitment to the IMF, as well as its voting power.” — International Monetary Fund.

The quota of SDRs held by countries reflects their voting powers at the IMF. In this manner, the IMF is similar to the Euro in approximating governance rights with skin in the game.

In addition to governance rights, the SDRs also bear interest. When a country holds more SDR than its allocated IMF quota, it receives interest on these holdings. In this sense, the SDR is unique. While it lacks the global utility of traditional currencies, it offers additional dimensions of global cooperation, and rewards users which participate in the currency.

When members of the International Monetary Fund have differences of opinion, they are able to exercise their voices by means of a voting system. As we’ve studied above, these voting systems aren’t necessarily in a ‘one person one vote’ structure — they recognize that some parties bear more risk in the system.

While currencies like the Euro, the Dollar and the SDR provide us with institutions to govern the global economy, their decision making powers are concentrated to a handful of mostly unelected delegates. Most importantly over the long term, while our existing currencies provide us with means of cooperation, fiat currencies are subject to debasement and political influence. This is why Bitcoin is such an economic innovation.

Bitcoin — A Digital Sound Money

“We don’t need a Fed. I have, for many years, been in favor of replacing the Fed with a computer”

Milton Friedman, 1999

Peter Thiel likes to say that there are ‘zero to one’ moments where we discover a truly new innovation. Bitcoin is such an invention.

Prior to 2008, there were many unsuccessful attempts at Digital cash, but the Bitcoin protocol is the first one that actually works without requiring a central facilitator. Even as we spend more of our lives online, prior to Bitcoin, every online transaction had to be settled using inefficient inter-banking arrangements, in currencies dictated by offline borders.

The invention of Bitcoin introduced the first borderless digital money which can be transferred peer to peer anywhere, without requiring any intermediaries. It can be hard to immediately comprehend the degree of innovation of Bitcoin, because it goes much further than a digital cash. The Bitcoin protocol also eliminates the need for correspondent banks to settle transactions, and the need for central banks to govern monetary policy.

When you send a wire to someone across the world, the money needs to hop across different correspondent banks before reaching your intended recipient, who likely has to wait a couple of days and incur foreign exchange fees in order to use the money in a different country. This changes with the advent of Bitcoin and cryptocurrencies, where money can now be exchanged directly between people without requiring a trusted third party.

In the coming years, traditional banks will incorporate blockchain technology to make their transaction settlements more efficient, but the currencies being transmitted through these new rails will retain the same inflationary designs of the last 100 years.

Building blockchain technology as a payment rail for legacy fiat currencies is like building roads and highways to ride horses. Technology rewards us when we embrace the potential of the future, not when we recreate the past.

Bitcoin reimagines money for the digital age, and also solves for inflation. Unlike fiat money, which can be printed at will, Bitcoin is programmed to be provably scarce. Bitcoin has a pre-determined monetary supply that is more scarce, divisible, and portable than our existing currencies. These characteristics makes Bitcoin a candidate for a new form of sound money — similar to a digital gold.

Much like gold is an apolitical physical commodity, Bitcoin aims to be an apolitical digital commodity. But Bitcoin is not just a physical commodity, it is also a software and a global network of voluntary users.

Over time, Bitcoin users will need to agree on approaches to upgrade this public infrastructure. Someone will need to type up new lines of code, someone else will need to review it, and as the network grows, users will need a means for dispute resolution when there are diverging viewpoints on any implementation.

Bitcoin users may not need to debate monetary policy, but they will need to agree on upgrades to Bitcoin as a software product.

Sound money needs to be durable, and the lack of a defined software upgrade process represents a long term risk for Bitcoin. In the near to midterm, Bitcoin’s lack of defined governance can be considered a positive feature, as it stabilizes the protocol from risky code changes. But software upgrades are an inevitability, not an option. The process for change doesn’t have to be undefined — it just needs to be methodical, and require a high bar of approval to ensure stability.

While our traditional currencies and financial systems are vulnerable to despots and depreciation, they provide us with a means of coordinating our voices. The lack of decision making framework represents a social threat to Bitcoin, as the currency does not provide its users with the same expression of voice provided by legacy institutions. If you don’t agree with a change in Bitcoin, the only means of dispute resolution is for users to exit the network.

The Bitcoin network has already seen community splits over different approaches to transaction settlement, and is poised to have contentious debates around privacy rules in the coming years. This is where Decred has an opportunity to shine.

Decred — An inclusive sound money

So far, this paper has examined money as a form of sovereignty, the pros/cons of central bank issued currencies, and an overview of how Bitcoin transforms monetary policy making and the legacy interbank settlement process.

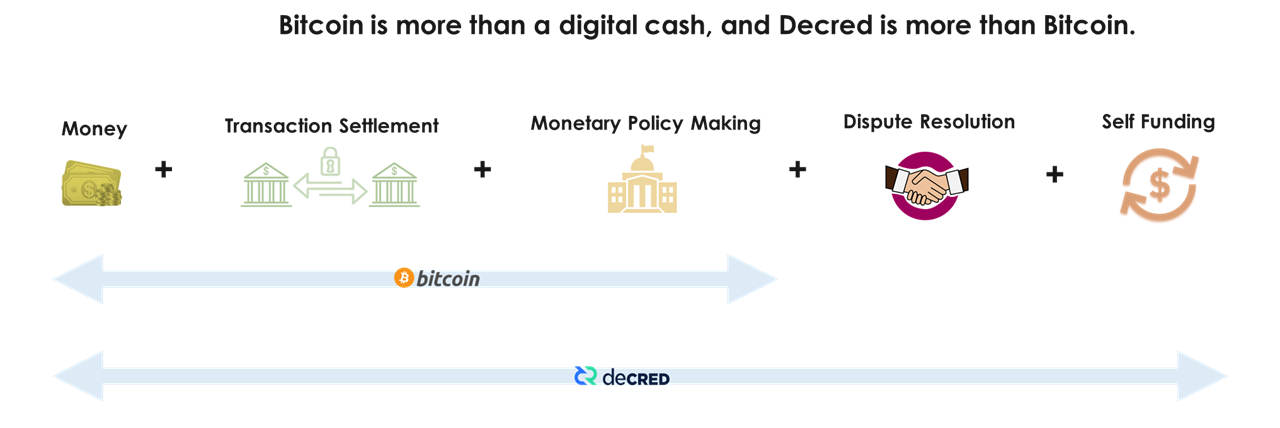

Decred is the same rabbit hole as Bitcoin, except its design extends in additional dimensions. While most cryptocurrencies are cheap imitations of Bitcoin, Decred specifically innovates in vectors not covered by Bitcoin’s design.

The 2008 creation of Bitcoin enabled a permissionless digital economy where anyone can exchange value, and where users are provided sound money guarantees against inflation. The 2016 innovation of Decred retains these same principles, and innovates in additional dimensions by empowering users with voice, and by solving for an ability to self finance an ecosystem without needing external investors.

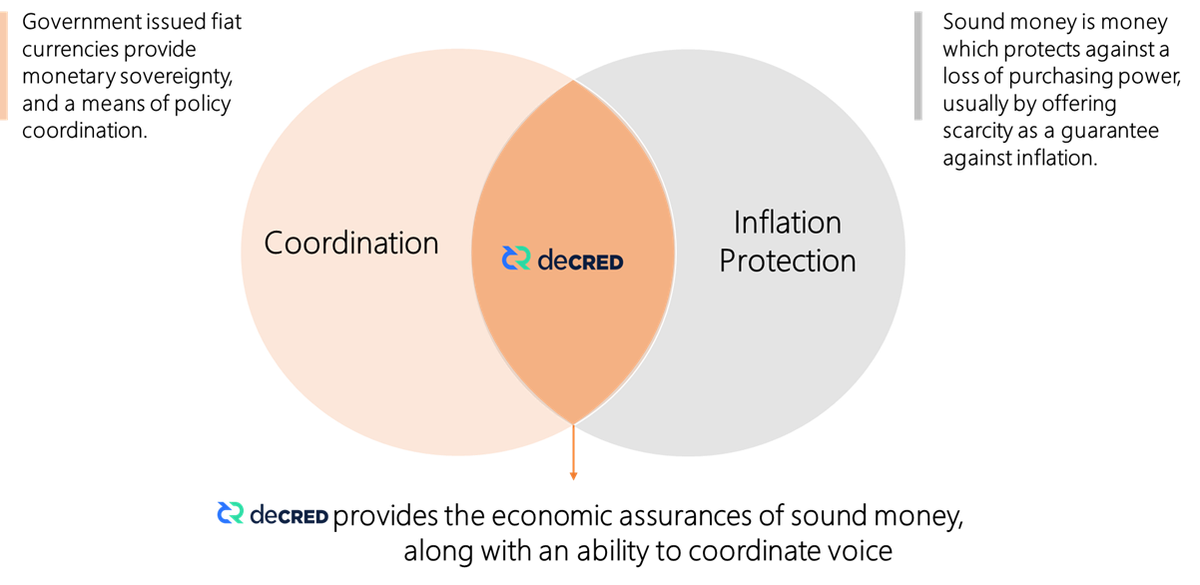

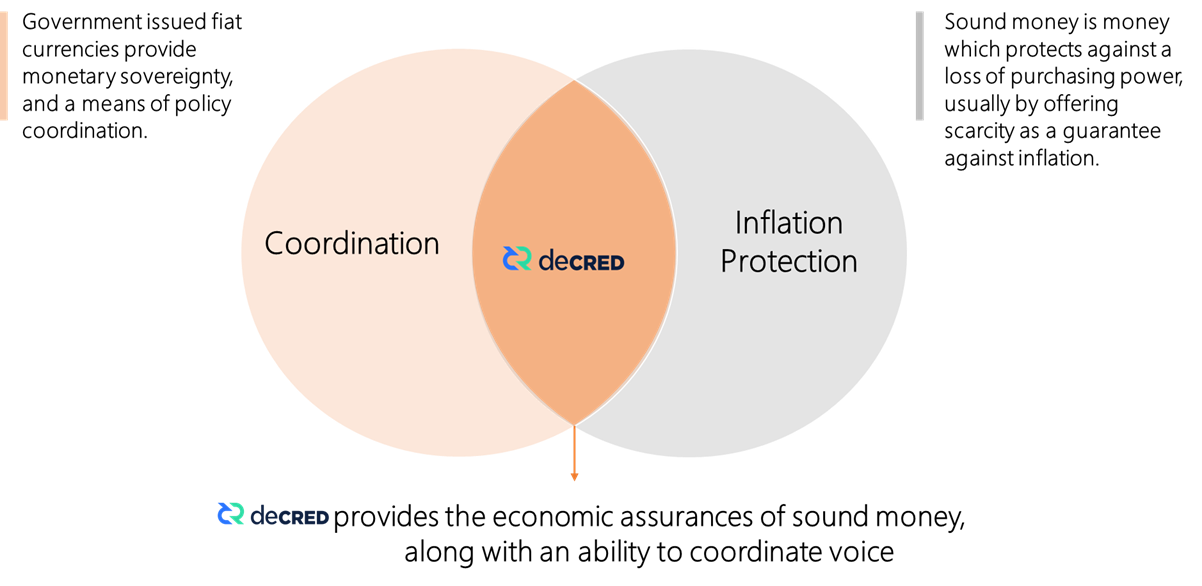

With Decred, we now have a means of retaining monetary hardness, while acknowledging that software products need a process for upgrades. More importantly as a monetary instrument, Decred not only provides the assurances of a sound money, it also provides users with a sovereign voice.

Decred was launched in 2016 with an explicit intent to extend the Bitcoin ethos of a global decentralized economy. Like Bitcoin, Decred also has a capped max supply of 21 million units, where each unit is divisible into 100 million decimal points. But there are notable differences in their design.

Decred is a cryptocurrency like Bitcoin, but Decred acknowledges a difference between economic soundness and technological malleability.

Decred doesn’t yet have the brand recognition of Bitcoin, but it is also very young. In terms of mined supply, Decred today is akin to Bitcoin in 2013.

Like Bitcoin, Decred doesn’t need central bank committees to debate monetary policy making. But while Bitcoin and Decred share economic similarities, they differ in the amount of voice afforded to the users of their currency.

Bitcoin’s design is similar to that of a digital gold. Decred’s design is something like a shareholders right on a digital gold.

Where Bitcoin’s design is apolitical and vague, Decred’s design embraces the fact that a sound programmable money needs to be both sound and programmable. More specifically, Decred automates politicking out of monetary policy making, but retains a framework for coordination and governance. It’s a currency without a single owner — a community where decision making is determined by distributed ownership.

“In complex domains, expertise doesn’t concentrate: under organic reality, things work in a distributed way, as F. A. Hayek has convincingly demonstrated… All we need is structure.

It doesn’t mean all participants have a democratic share in decisions. One motivated participant can disproportionately move the needle…But every participant has the option to be that player.

Which is why Bitcoin is an excellent idea. It fulfills the needs of the complex system, not because it is a cryptocurrency, but precisely because it has no owner, no authority that can decide on its fate. It is owned by the crowd, its users…For other cryptocurrencies to compete, they need to have such a Hayekian property.”

Nassim Nicholas Taleb, January 22, 2018.

Nassim Taleb wrote the above words as a foreword for The Bitcoin Standard, one of the most well known Bitcoin books to date. Arguably, these words are a better descriptor of Decred.

Decred has no single owner — It is owned by the crowd.

Where traditional currencies are governed by central banking committees, Decred is governed by the public. In many ways, Decred combines the economics of Bitcoin with governance structures similar to the original ambitions of the Special Drawing Rights.

Like the Special Drawing Rights, Decred assigns governing rights to those who have the most skin in the game. But where SDRs are limited for use by international institutions, Decred is a digital public currency that is open to all. Where the SDR uses a basket of currencies to come up with an asset value, Decred has a native currency, $DCR. The SDR basket suffers from a politicization problem, where every 5 years there is lobbying amongst countries (most recently by China) to reshuffle the currency basket in their favour. Decred’s design throws out the proxy basket model, and replaces it with a new currency altogether.

Until now, a history of human governance models relied on kingdoms and delegated leaders. For the first time, we have a model of economic governance where every individual is free to participate in a global decision making process. In addition to giving input into the evolution of the software, Decred holders also dictate the allocation of the currency’s treasury fund.

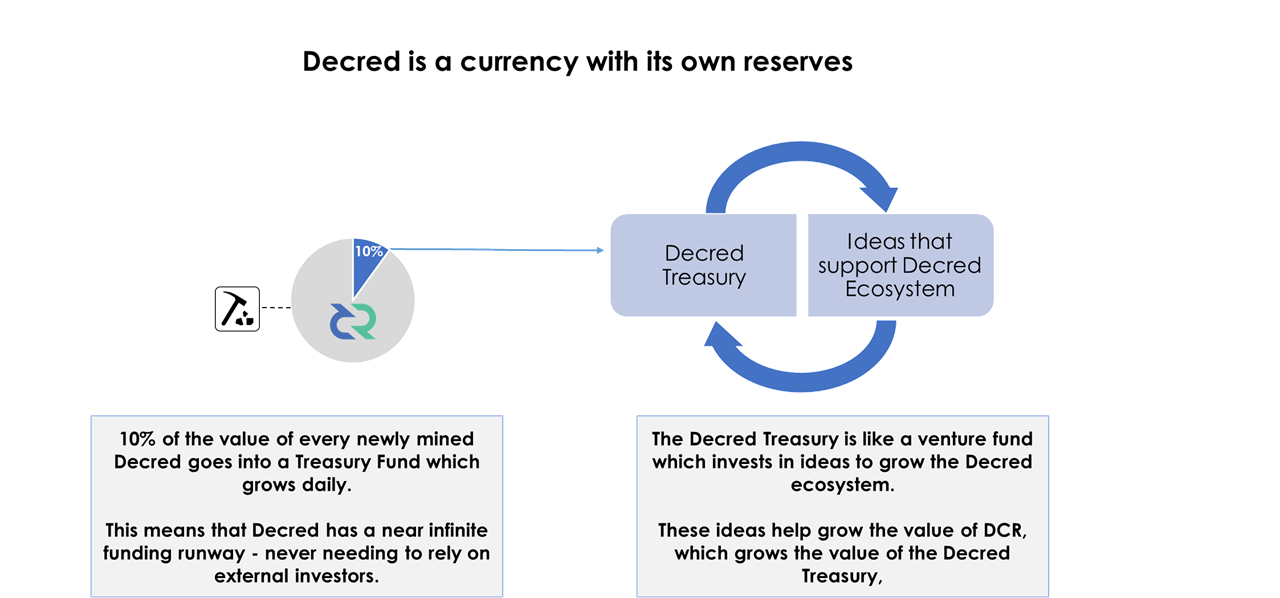

Decred is a currency with its own reserves.

One of the most interesting innovations for Decred is the ability to fund its own treasury. At a time of populism when international organizations often bicker about contributions to collective funding, Decred is a financial network which has to depend on outside investors to develop its ecosystem.

In my 2019 paper “An Alternative Contender”, I studied how the Treasury Fund is funded by directing a portion of $DCR mining rewards towards a community pool, and how this pool has the potential to become a war chest in the future. As long as someone around the world is willing to mine $DCR, the treasury will continue to fund itself.

Self sustenance is a pre-requisite for any decentralized currency to succeed long term. Yet most cryptocurrencies rely on external investors to fund their development. Self funding can never be added to Bitcoin, and it will always remain dependent on voluntary donations. This may not be an obvious risk today, but clear community governance and self funding are two dimensions that can never be added to Bitcoin’s design.

On the contrary, Decred is designed to be self sustainable. Having a treasury means the Decred protocol can invite developers and community contributors without being bound to external interests. Longer term, this also prevents a risk where a shared commodity succumbs to a tragedy of the commons.

Decred is also designed to reward loyalty. If you are willing to hold Decred for up to 142 days, you can participate in the Decred staking process. This means you can earn a yield on the currency, similar to how the IMF pays interest for holding SDR quotas. This staking reward will go down over time, which is designed to reward the early adopters who take on the most risk. More than half of the $DCR mined to date are locked into its governance staking system, which shows early signs of a product-market fit. It’s noteworthy that such a large number of users lock up their $DCR for months at a time, knowing that cryptocurrency prices fluctuate on a dime.

Decred now has a track record of 4 years. It may not yet have the brand recognition of other currencies, but its design is structured for long term durability and powerful network effects.

Weaknesses, Misconceptions and Opportunities for the future:

- Decred has low brand name recognition, and it can be complex to understand: The biggest near term challenge with Decred is a lack of mainstream awareness. While Bitcoin (and to a lesser extent Ethereum) have gained global recognition, Decred’s awareness is concentrated in cryptocurrency circles. Most of the world is only beginning to understand the value proposition of Bitcoin, and Decred’s value prop is a deeper extension of that rabbit hole. Bitcoin innovates on fiat currencies, and Decred innovates on Bitcoin. This thesis will take a long time to play out, and we are still in the early days.

- Regulatory risk: This risk applies to most cryptocurrencies, but it’s worth noting that Decred hasn’t passed the same regulatory scrutiny that Bitcoin has. The US Securities and Exchange Commission (SEC) has already ruled that Bitcoin is not a security, and Decred would benefit from such reassurance. Decred’s design is unique in that it is more than a traditional currency — it also offers interest yield, and provides governance rights over a shared community collective. Decred may need to draw parallels with the Special Drawing Rights to show how currencies can be more than utility tokens. If Decred were to become a serious alternative to national currencies, a regulator may try to enact adversarial laws to limit its adoption. It is also worthwhile to note that offline laws can’t shutdown the Decred network. As long as it is profitable to mine $DCR, someone somewhere will continue to support the Decred network. This resilience may ultimately be Decred’s best defense over the long term.

- The rich hold the most sway: It’s true that Decred rewards voice to those who hold the most $DCR, but the governance process is specifically designed with checks and balances. Let’s examine how Decred solves for a risk of concentration of power:

- Dilution of the early holders: The rich don’t just get to keep their voice. As more Decred gets mined, the voice of the early holders get diluted. This process will continue until all 21M $DCR has been mined, which will take place over many decades. This dilution ensures a check and balance to eliminate the privileges of early Decred holders. If the early adopters want to hold onto their voice, they will need to buy back in alongside everyone else.

- Skin in the game: Skin in the game is a necessary practice to ensure a fair distribution of risk. Decred’s method of governance makes it transparent to rewards measurable risk in its ecosystem. Most importantly, governance is open to all. This paper analyzed how our existing currency governance structures are already structured around skin in the game. Decred makes this processes fairer, because voting power is no longer limited to a small group of delegates. Anyone has a chance, if they’re willing to take on risk.

- High thresholds for consensus: One of the biggest features of Decred’s governance system is that it’s not enough to hold the most $DCR. A super majority of the ecosystem needs to agree. Stability is an important feature for a sound currency. Decred’s design makes it possible to change, but difficult to do so. Decred’s governance structure requires super majority approvals from the holders of the currency, as well as those who have invested in mining hardware. In some ways, this governance structure is similar to that of the IMF, where major decisions require an approval from 85% of its members.

5. Distributed global governance is a new experiment. Global direct governance is a rethinking of so many of our existing societal structures. Bitcoin unbundles our offline institutions from governing an online money. Decred rebundles money and governance, in a digitally native state. This will have profound implications, including losing some of our traditional national safety nets. Ultimately, decentralization empowers more people, but this progress comes with uncertainty and bumps. The economic impact of cryptocurrencies will be analogous to the social impact of the printing press. In ancient times, literature was limited to printing by select decree. The spread of the printing press and eventually the internet have made it possible for anyone to share information with the world. This process has empowered more people with a voice than ever before in history. But as social media has shown, too many voices can also create noise. Decred’s treasury fund offers a means of self financing, but the allocation of these resources will likely lead to community disagreements. Those whose voice is rejected may feel more disheartened than if they never had that voice in the first place.

Decred gives us a structure for organizing around a shared digital economy, but we don’t yet know what those structures will end up looking like.

Conclusion:

Our money is rapidly transforming from physical to digital format. Once all currencies are digitized, online money will decouple from offline borders. Bitcoin has captured mainstream attention as a decentralized digital inflation-proof money, and Decred extends this design further.

The future of money is digital. If Bitcoin is a digital sound money, Decred is sound money with voice.

Acknowledgements: I want to thank Permabull Nino, Checkmate, Richard Red, Mrbulb, and Elian for being kind enough to proof read earlier versions of this article.

Disclaimer: This article is meant for informational purposes, not as professional investment advice.

{kind=link}

Comments ()